Mergers

Both the existing and new owners must ensure that the information concerning the employment relationships is linked to the correct sub-entity.

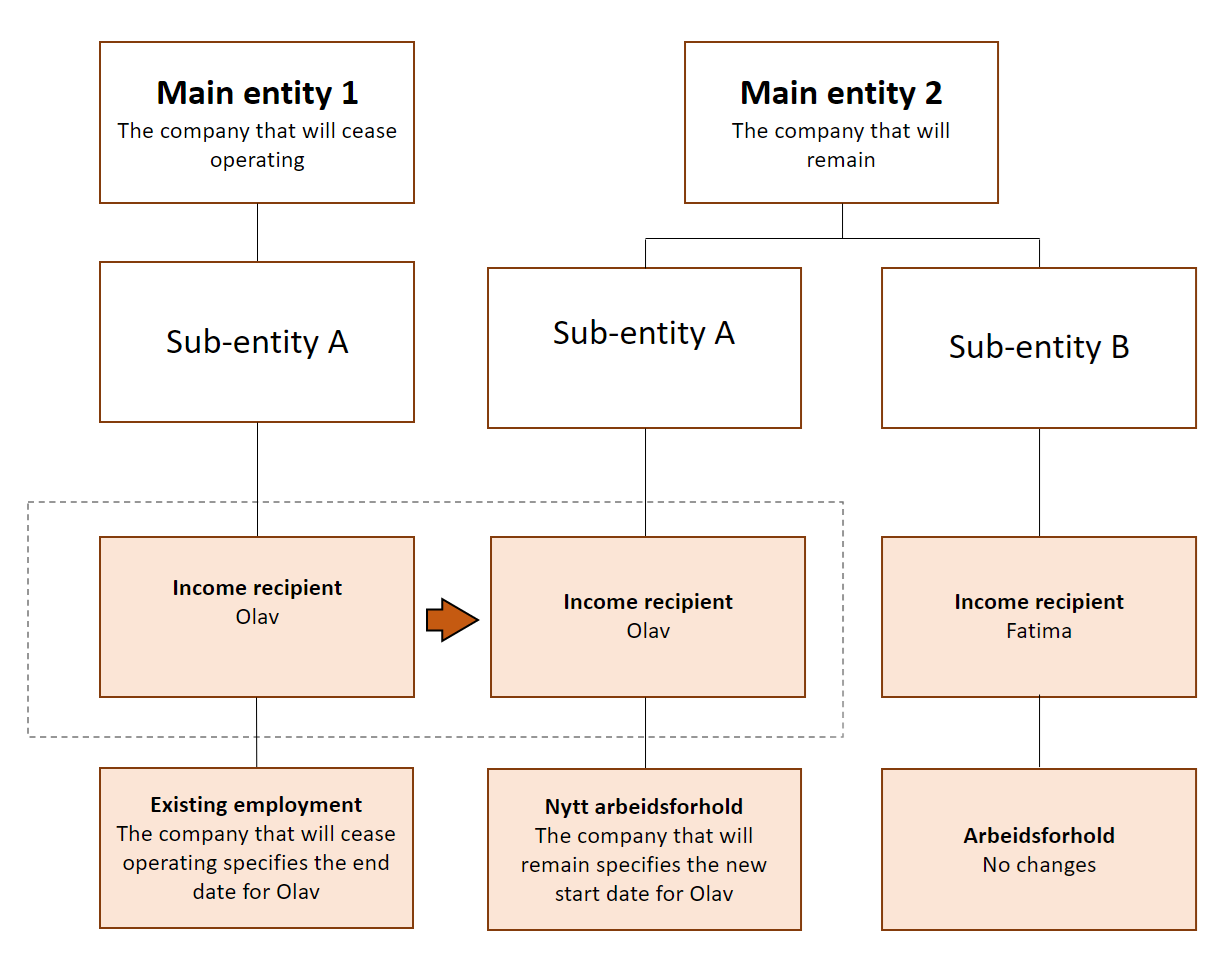

A merger occurs when two or more main entities merge to form a single company. One company (the acquiring main entity) takes over the business of one or more companies (the divesting main entity).

What you have to do

- The divesting main entity report an end date and cause of end date for all employment relationships

- The acquiring main entity report start date for all new employees

Divesting main entities must specify the end date for the employment relationships concerned

As a divesting main entity, you must report an end date and as cause of end date changes in organisational structure or internal job swap for all employment relationships.

Example

Divesting company, main entity 1, must terminate all employment relationships because they have been merged into main entity 2. Main entity 2 takes over main entity 1 with effect from 1 June.

| A-melding for May | |

| Main entity | 1 |

| Sub-entity | A |

| Income recipient | Olav |

| Employment start date | 1 January |

| Employment end date | 31 May |

| Cause of end date | changes in organisational structure or internal job swap |

They also enter the other mandatory information.

Acquiring main entity must specify a start date for the new employment relationships

As the acquiring main entity, you must report employment relationships for all employees for whom you take over employer responsibility. For a more detailed explanation of the information that you must provide, see the various types of employment.

Note!

The new start date for the employment must be the day after the end date, in order for the information in NAV’s Aa Register to be correct. For example, end date of 31 May and start date of 1 June.

Example

The acquiring company, main entity 2, must specify all employment relationships from the date on which they take over employer responsibility for the employees of main entity 1.

| A-melding for June | |

| Main entity | 2 |

| Sub-entity | A |

| Income recipient | Olav |

| Employment start date | 1 June |

| Employment end date | |

They also enter the other mandatory information.